EIT Climate-KIC is exploring challenge of redesigning venture capital

EIT Climate-KIC’s Transformation Capital is an experimental initiative uncovering why the current economic system isn’t working for people or the environment.

It aims to uncover the axioms, paradigms, and structures belonging to a just, ecological economy. For the past nine years, EIT Climate-KIC has supported over 1 600 climate-positive start-ups in 31 countries. These companies have gone through the EIT Climate-KIC Accelerator, a three-stage program providing financial support, training, tools, and coaching. Collectively, they have raised more than EUR 1 billion in venture capital. Some of EIT Climate-KIC most notable alumni include Ynsect, tado, Lilium Aviation, Volocopter, Thermondo, and Climeworks.

Greenhouse gas emissions continue to rise

As impressive as these numbers are, they cannot mask the fact that greenhouse gas emissions continue to rise. Many of the companies in the EIT Climate-KIC portfolio are working on important building blocks of a sustainable future, such as insect-derived proteins, smart thermostats, and electric transportation. Yet, climate change is no longer a problem of technology development—it is one of technology diffusion.

None of these start-ups has so far succeeded in changing the structural fabric of the economy. Nor has any of them managed to unleash the type of dynamics required for responding to the IPCC’s call for the 'rapid, far-reaching, and unprecedented' transformation of human systems.

EIT Climate-KIC isn’t alone in having this problem. Venture capitalists have poured billions into the clean-tech sector but have little to show for it in terms of sending the world down emissions reduction trajectories aligned with the goals of the Paris Agreement.

Some may argue that the challenge EIT Community faces is too colossal for any single start-up. They may add that start-ups are here to create optionality for society but that people must ultimately choose their own future through their choices in elections and in supermarkets. Both of these objections are valid. Yet, it is the mechanism through which the EIT Community provides risk capital—the lifeblood of entrepreneurial endeavours—that prevents us from fully leveraging the power of entrepreneurship. This mechanism biases the start-up selection process towards market conformance. It breeds optionality that is incremental, not transformative.

If the EIT Community doesn’t succeed at reprogramming the 'deep code' of society—and along with it entrepreneurial finance— the EIT will end up with fantastically smart devices but use them only to predict the next searing heat waves and torrential floods instead of preventing them.

The problem with traditional venture capital

Venture capital (VC) is the primary mechanism through which entrepreneurial finance is supplied to the economy. Today’s VC sector—like capital markets at large—operates under a set of axioms, paradigms, and structures that inhibits its ability to have systems-transformative effects.

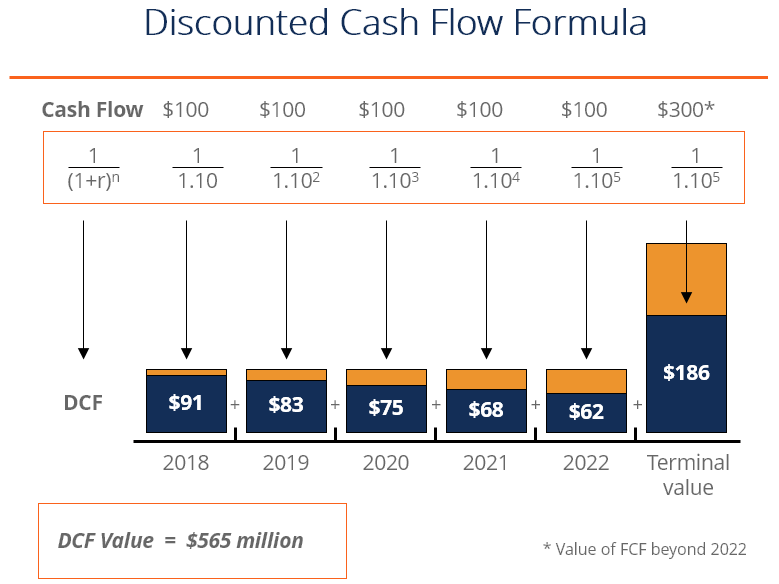

Discounted Cash Flow

The Discounted Cash Flow method is based on traditional asset pricing theory, which states that the value of an asset is equal to the sum of all future net cash flows discounted at a risk-appropriate rate. When assessing the attractiveness of a start-up, VCs ask a capital-raising entrepreneur to forecast the net cash flow of her company three to five years into the future. The VCs assume that the company will ‘exit’ either through a trade sale or an initial public offering. At such a ‘liquidity event’, someone is expected to pay a multiple of the company’s profitability—as measured, for instance, by EBITDA—in return for equity.

An example of how the Net Present Value—the sum of all discounted free cash flows — is calculated using the DCF method, assuming a 10 per cent discount rate. (Credit: CFI)

DCF as a primary decision-making and accountability framework

First, the DCF only considers values that are captured by today’s accounting standards. The need to evolve these standards—and the value frameworks they are based upon, such as GDP—has long been recognised, even amongst VCs. But as long as VCs and their investors are being held accountable by today’s accounting principles, they won’t adopt valuation paradigms that capture positive externalities such as climate resilience and social cohesion.

Second, the DCF forces companies to sell into already existing markets. Otherwise, how would they be able to show a positive EBITDA in five years? The DCF favours business models that fit into the existing industrial structure, not those that promise to transform it.

This is also true for many start-ups labelled ‘disruptive’, such as Uber and Airbnb. These start-ups might disrupt the behaviour of consumers and the business of competitors, but they rarely transform the economic structures and paradigms that shape an industry.

'Disruptive’ start-ups of the 21st century

Uber and Airbnb are amongst the most ‘disruptive’ start-ups of the 21st century. As pioneers of the sharing economy, they even made the Global Cleantech 100. Yet their net environmental footprint is dismal. Uber has been shown to cause more congestion and to undermine public transport. Airbnb has fueled an expansion of the lodging market. Whilst Airbnb rooms often have lower environmental footprints than hotels, rebound effects are common.

Another reason why the DCF inhibits truly transformative investing is that it imposes an artificial execution timeline on start-ups. Because VCs promise their investors to return capital within seven to ten years, each start-up must show a viable pathway to exit within three to five years. This means that business plans cannot be tailored to what’s sensible for a given innovation. Instead, they must conform to the arbitrary investment cycle of the VC asset class. A case in point is the frenetic land-grabbing tactic employed by electric scooter companies like Lime and Bird.

Like any incarnation of the sharing economy, e-scooters hold great promise to reduce carbon emissions. However, the paradigms of today’s venture capitalists force start-ups to pursue unsustainable execution strategies, all but ensuring that this promise will never be realised. (Credit: Kristen Rogers via CURBED)

Unsustainable return expectations

Finally, the DCF raises unsustainable return expectations. A start-up must show how it might conceivably score an exit multiple of 10x to give VCs a chance to generate a 20–30% return on investment for their portfolio as a whole. Yet those expectations rest on the historical performance of the asset class—on the companies that have extracted value above the rate afforded by the Earth’s planetary boundaries, the companies that got us into this mess in the first place. This includes software companies whose revenue model relies on online advertising and thus on the perpetuation of consumerism—a root cause of climate change—such as Facebook, Google, and Twitter.

What drives the continued use of the DCF amongst clean-tech VCs and impact investors is the myth of green growth, the idea that people can decouple economic activity from carbon emissions so that people can green our society and continue consuming. Unfortunately, there is no evidence of the possibility of long-term absolute decoupling within the existing economic model. So as long as the venture capital community adheres to the above paradigms, it will fail to generate meaningful climate impact.

Why entrepreneurial finance is critical to address climate change

The popular discourse often equates entrepreneurship with start-ups. In the context of complex challenges such as climate change, this equation isn’t useful.

Entrepreneurship is an innovation practice—a collection of particular mindsets and approaches to solving specific problems. The nature of this innovation practice is one of experimentation. Experimentation matters because complex adaptive systems—such as the economy and the Earth’s climate — are non-deterministic systems whose evolution cannot be precisely forecast, let alone tightly controlled. People simply don’t know how to build a low-carbon, climate-resilient world. Experimentation is thus the most promising strategy for exploring viable pathways to alternative futures.

Entrepreneurship as practice of innovation

In the EIT Climate-KIC’s systems innovation model, entrepreneurial initiatives play an important part as the ‘supply-side’ of innovation. EIT Climate-KIC considers entrepreneurship as a practice of innovation that has important applications in all levers of change—not just technology. (Credit: EIT Climate-KIC)

The ‘start-up’ is one of several ways in which entrepreneurship can manifest itself. At its core, it is a legal wrapper that allows entrepreneurs to coordinate work, raise capital, and protect their liability. The problem is that the idea of a start-up is now a mental model so rigidified by homogeneous paradigms, heuristics, and expectations of venture investors that it loses its transformative power. In order to fit in, start-ups must conform to the cookie-cutter world of investors.

Yet to cope with the greatest challenge humanity has ever faced, cookie-cutting won’t work. There are two ways out of this predicament. The first is to change the rules of the game of entrepreneurial finance. The second is to reimagine the start-up, to liberate it from the straightjacket of traditional VC so that entrepreneurship can manifest itself again in more varied and sophisticated forms.

The challenge of redesigning venture capital

The challenge the EIT Community needs to solve is to direct entrepreneurial finance in a way that promises to produce systems-transformative dynamics. Specifically, the EIT Community must design an approach capable of supporting initiatives that may:

- Address no existing market and therefore cannot forecast net cash flows

- Take more than three to five years to achieve scale

- Follow non-commercial impact pathways

- Engage the properties of complex adaptive systems (such as emergence)

- Forge unusual partnerships with the public and philanthropic sectors

- Modify the typical management+board governance formula

- Choose legal structures other than the limited liability company

- Generate value beyond what’s captured by today’s accounting standards.

What EIT Climate-KIC knows is that what’s laid out above doesn’t mean all risk capital needs to be concessional or philanthropic. EIT Climate-KIC believes it’s possible to generate meaningful climate impact alongside a viable financial return. But EIT Climate-KIC thinks it’s time to readjust return expectations, letting go of the idea that venture capital—impact-oriented or not — should achieve financial ROI at the same level the asset class has reached during its extractive, unsustainable past.

EIT Climate-KIC also thinks that it needs to redefine the meaning of ‘climate impact’ for the asset class. The impact must no longer be understood purely in terms of potential carbon emissions savings on a unit-level. Such a narrow, inherently unsystematic framing biases VC portfolios towards incremental solutions that may represent low-carbon alternatives to incumbent technologies but perpetuate the existence of our consumerist industrial system.

Finally, redesigning entrepreneurial finance isn’t just a question of what to invest in—but also of the how and the who of making these investments. What paradigms does EIT Climate-KIC operate under? What norms and values does EIT Climate-KIC apply? Which actors of society does EIT Climate-KIC involve? What decision-making and accountability frameworks does EIT Climate-KIC use? How does EIT Climate-KIC unlock new sources of value and make them transactable?

These are some of the questions EIT Climate-KIC is exploring as part of the Transformation Capital initiative. So far, EIT Climate-KIC has no answers. What EIT Climate-KIC does have is a nine-year track-record of incubating and accelerating climate-relevant start-ups. Now EIT Climate-KIC needs help in redesigning entrepreneurial finance.

Share this page

Share this page